Who Google AI Mode actually cites when Indonesians ask about banking.

// table_of_contents▸

- 1.Banks own most of the answer

- 2.The single most-cited site is not a bank

- 3.Where you are in the journey changes who wins

- 4.Loans, savings, and cards each attract a different crowd

- 5.The brands AI Mode names most

- 6.The citations move every time you ask

- 7.What this means if you want to get cited

- 8.How we ran this

Google AI Mode now sits at the top of more and more banking and finance searches in Indonesia, answering the question before anyone reaches a website. That raises a practical problem for any bank, lender, or fintech that cares about being found, because when an Indonesian asks AI Mode about a mortgage, a savings account, or a credit card, someone’s website is being quoted back as the answer. We wanted to know whose, so we measured it instead of guessing.

We wrote 72 prompts in Bahasa Indonesia across three areas, home and personal loans, savings and deposits, and credit cards, and split them by where a buyer sits, from broad awareness questions through to branded, ready-to-apply queries. Each prompt ran three times through the Google AI Mode API with Indonesian localisation, which gave us 216 separate answers and 2,068 citations spread across 312 different domains. Every cited link was tagged by the kind of organisation behind it, so we could see the real shape of who AI Mode trusts in this market.

Banks own most of the answer

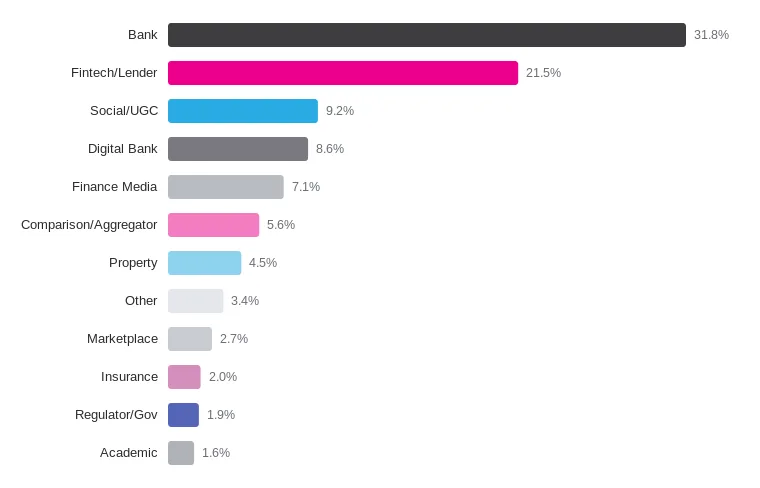

Across every query we tested, the pattern held. Banks supply the largest share of what AI Mode cites, 31.8% of all citations on their own. Fold in the digital banks like blu and SeaBank and the banking sector reaches 40.4%, and once you add the fintech lenders and paylater apps, first-party financial institutions account for close to 62% of everything AI Mode quotes. In Indonesian finance, AI Mode treats the company’s own website as the primary source of truth.

Independent finance media is far smaller than most people assume, at 7.1%, and comparison sites sit at 5.6%. The real surprise is social content, which at 9.2% outweighs the news outlets, carried almost entirely by Instagram, YouTube, and TikTok. Regulators barely register, with OJK, Bank Indonesia, and LPS together making up 1.9% of citations and only about one answer in nine referencing a regulator at all, even on questions where the regulator is the actual authority. So when a brand’s own pages are thin, AI Mode does not reach for a newspaper to fill the gap, it reaches for a comparison marketplace or a creator’s Instagram post.

Share of all AI Mode citations by source type (n=2,068 citations).

Share of all AI Mode citations by source type (n=2,068 citations).

| Source type | Share of citations |

|---|---|

| Bank | 31.8% |

| Fintech/Lender | 21.5% |

| Social/UGC | 9.2% |

| Digital Bank | 8.6% |

| Finance Media | 7.1% |

| Comparison/Aggregator | 5.6% |

| Property | 4.5% |

| Other | 3.4% |

| Marketplace | 2.7% |

| Insurance | 2.0% |

| Regulator/Gov | 1.9% |

| Academic | 1.6% |

The single most-cited site is not a bank

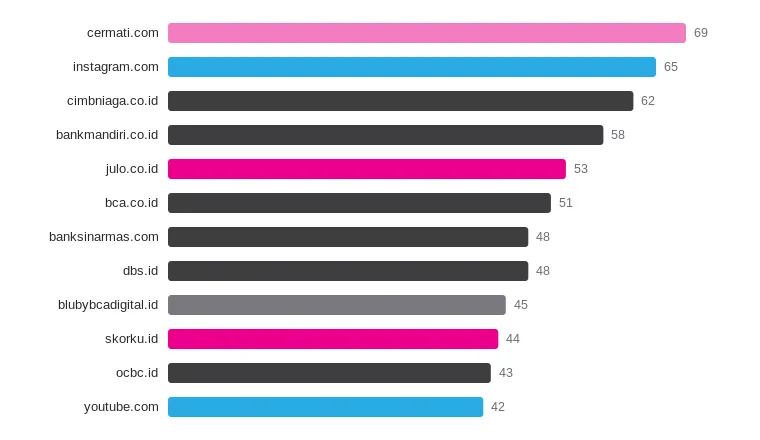

For all the bank dominance in aggregate, the most-cited individual domain belongs to none of them. It is Cermati, a financial comparison site, which shows up in 26% of every answer we collected. Right behind it is Instagram, cited in 24% of answers, ahead of every single bank, and the first bank domain on the list, CIMB Niaga, only comes third.

The credit-score apps are the other standout. Skorku, Skorlife, and IDScore all rank far higher than their category size would predict, because they publish a deep library of plain-language articles about loans, eligibility, and credit health, which is exactly what AI Mode is trying to answer. What earns them the citations is the volume and structure of their educational content rather than the size of the brand.

The 12 most-cited domains across 216 answers.

The 12 most-cited domains across 216 answers.

| # | Domain | Source type | Citations | Share |

|---|---|---|---|---|

| 1 | cermati.com | Comparison/Aggregator | 69 | 3.3% |

| 2 | instagram.com | Social/UGC | 65 | 3.1% |

| 3 | cimbniaga.co.id | Bank | 62 | 3.0% |

| 4 | bankmandiri.co.id | Bank | 58 | 2.8% |

| 5 | julo.co.id | Fintech/Lender | 53 | 2.6% |

| 6 | bca.co.id | Bank | 51 | 2.5% |

| 7 | banksinarmas.com | Bank | 48 | 2.3% |

| 8 | dbs.id | Bank | 48 | 2.3% |

| 9 | blubybcadigital.id | Digital Bank | 45 | 2.2% |

| 10 | skorku.id | Fintech/Lender | 44 | 2.1% |

| 11 | ocbc.id | Bank | 43 | 2.1% |

| 12 | youtube.com | Social/UGC | 42 | 2.0% |

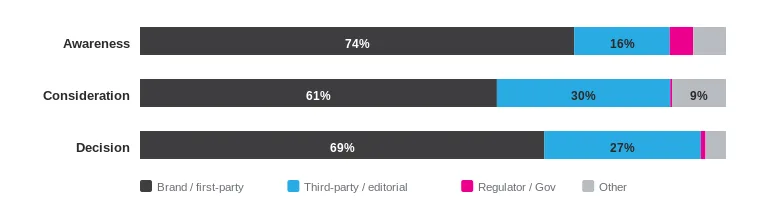

Where you are in the journey changes who wins

The most useful pattern in the data appears when you split citations by buyer stage. For broad awareness questions like what is a KPR or how paylater works, brand-owned sites dominate at 74%, because AI Mode explains the basics by quoting the banks and lenders themselves. At the decision stage, where the query already names a brand, first-party sites lead again at 69%, since a search for how to open a SeaBank account naturally pulls SeaBank’s own pages.

The consideration stage behaves differently, and it is the one that matters most commercially. When someone asks which bank has the cheapest mortgage or the best digital bank for saving, third-party and editorial sources jump to nearly 30% of citations, comparison sites climb to 7%, and social content reaches almost 13%. Fintech sites even overtake banks here, taking 24.3% of citations against the banks’ 22.7%. This is the moment a customer is choosing between providers, and it is where a brand that only optimises its product and application pages loses the conversation.

| Buyer stage | Brand / first-party | Third-party / editorial | Regulator / Gov | Other |

|---|---|---|---|---|

| Awareness | 74.1% | 16.3% | 4.0% | 5.6% |

| Consideration | 60.9% | 29.6% | 0.3% | 9.2% |

| Decision | 69.0% | 26.7% | 0.8% | 3.5% |

A bank can be everywhere in the awareness and decision answers and still be missing from the comparison that decides the sale. That gap is where most of the AI-search opportunity sits right now.

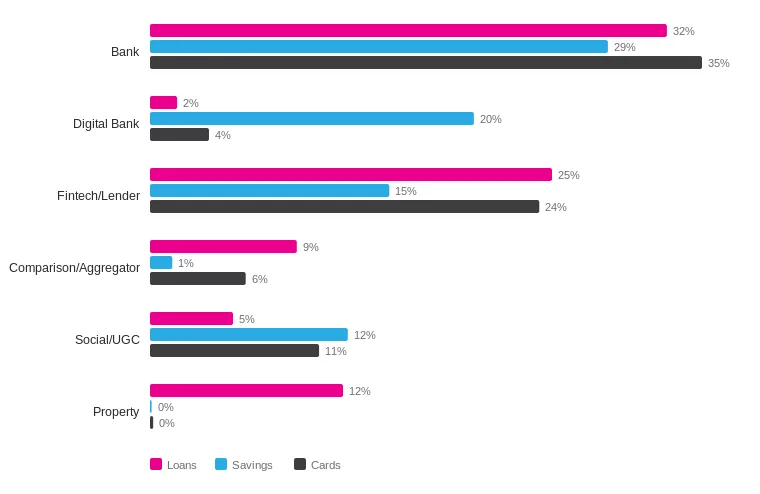

Loans, savings, and cards each attract a different crowd

The mix shifts by product as well. Loan answers pull in the widest range of sources, with property portals and developers taking 12% of loan citations as AI Mode reaches for housing listings alongside the bank pages, and comparison sites adding another 9%. Savings and deposits is the category where digital banks surge to 20% of citations and where social content climbs to 12%, a sign that the digital-first savings race is being narrated as much on Instagram and TikTok as on any bank site.

Cards are the most bank-controlled of the three, with issuer sites and card microsites doing most of the talking and fintech and social filling the rest. If you work in lending or deposits, the read is that your competition for a citation is not only other banks, it is comparison sites, property portals, and creators.

Source-type mix within each product area.

Source-type mix within each product area.

| Source type | Loans | Savings | Cards |

|---|---|---|---|

| Bank | 32.4% | 28.7% | 34.6% |

| Digital Bank | 1.7% | 20.3% | 3.7% |

| Fintech/Lender | 25.2% | 15.0% | 24.4% |

| Comparison/Aggregator | 9.2% | 1.4% | 6.0% |

| Social/UGC | 5.2% | 12.4% | 10.6% |

| Property | 12.1% | 0.1% | 0.2% |

The brands AI Mode names most

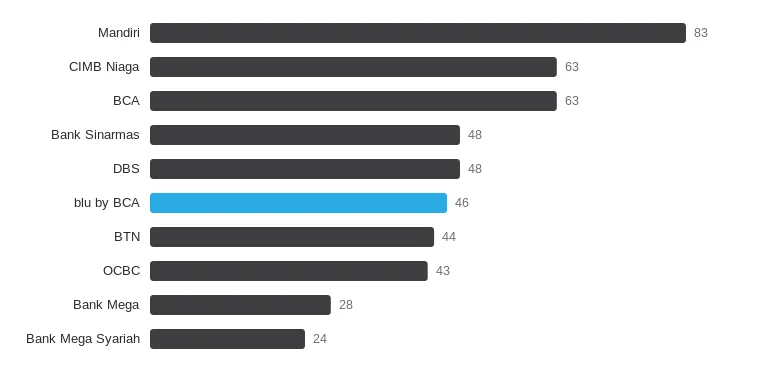

Among banking brands, Bank Mandiri, CIMB Niaga, and BCA are cited most often through their own domains, with blu by BCA and SeaBank leading the digital banks. CIMB Niaga is the clearest over-performer relative to its market share, and the reason is its large library of educational inspirasi articles that AI Mode quotes again and again.

Banks and digital banks cited most, by own-domain citations.

Banks and digital banks cited most, by own-domain citations.

| Bank / digital bank | Own-domain citations |

|---|---|

| Mandiri | 83 |

| CIMB Niaga | 63 |

| BCA | 63 |

| Bank Sinarmas | 48 |

| DBS | 48 |

| blu by BCA | 46 |

| BTN | 44 |

| OCBC | 43 |

| Bank Mega | 28 |

| Bank Mega Syariah | 24 |

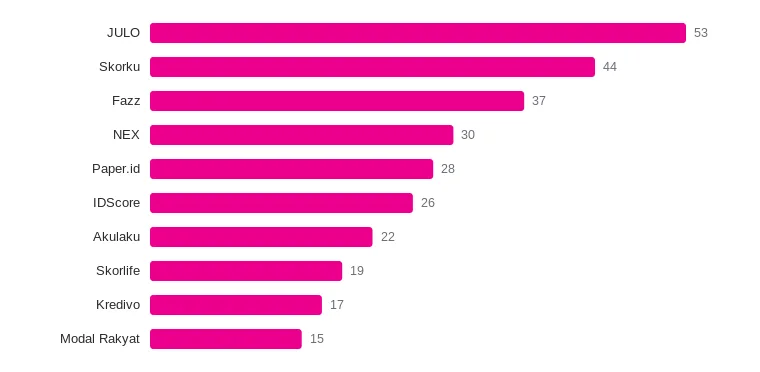

On the fintech side JULO is well ahead of the field, followed by the credit-score apps and payment players like Fazz and Paper.id. None of them earn their place through glossy product pages, but through the sheer volume of well-structured explainer content aimed at the loan and credit questions people actually type.

Fintech and lender brands cited most, by own-domain citations.

Fintech and lender brands cited most, by own-domain citations.

| Fintech / lender | Own-domain citations |

|---|---|

| JULO | 53 |

| Skorku | 44 |

| Fazz | 37 |

| NEX | 30 |

| Paper.id | 28 |

| IDScore | 26 |

| Akulaku | 22 |

| Skorlife | 19 |

| Kredivo | 17 |

| Modal Rakyat | 15 |

The citations move every time you ask

Because we forced a fresh answer on every call rather than a cached copy, we could measure how stable AI Mode is, and it is not very stable. Across three runs of the same prompt, only about half the cited domains stayed the same from one run to the next, a Jaccard overlap of 0.51. The number of sources per answer swung just as widely, from a single citation to 26 in one response.

For anyone tracking visibility, that volatility is the real lesson. Checking once whether AI Mode cites you tells you almost nothing, because the same query can cite you now and skip you on the next pass. Visibility here has to be measured as a rate across many repeated queries over time, which is how this study was built and how ongoing monitoring should work.

What this means if you want to get cited

The first move is the most obvious and the most underused. With roughly 62% of citations going to financial institutions’ own domains, a deep, well-structured educational hub on your own site is the highest-return work available, and CIMB Niaga and JULO are proof that a serious content library converts directly into AI Mode citations.

The second is to fight for the consideration stage on purpose. That is where comparison sites and social content take a third of the citations, so publishing honest comparative content, the best card for cashback or the cheapest mortgage for a given salary, and earning a presence on the comparison marketplaces that already rank, is how you claim that space back.

Social deserves to be treated as a citation channel and not only a reach channel, since Instagram, YouTube, and TikTok are cited in roughly a quarter, an eighth, and a tenth of answers. There is also a clear opening around tools and eligibility content, where the credit-score apps have shown that utility paired with education earns outsized visibility. None of it works as a one-off, so track your share of voice across repeated prompts rather than trusting a single check.

How we ran this

The study covers 72 Bahasa Indonesia prompts across loans, savings, and cards, each run three times through the Google AI Mode API with Indonesian localisation and caching turned off, for 216 answers collected in July 2026. We classified all 312 cited domains by organisation type through a mix of rules and manual review, leaving a small 3.4% other bucket for the B2B and infrastructure sites that do not fit a category.

This is a directional snapshot rather than the last word. AI Mode is non-deterministic, so the exact percentages will shift on a re-run, but the structure holds, the bank dominance, the consideration-stage swing toward third parties, the strength of social, and the near-absence of regulators. The full domain leaderboard and every raw citation sit in the dataset behind this piece.

See where your brand stands in AI answers today, benchmarked against your competitors, no pitch required.

Your content can sit inside two billion AI answers a month and still send zero visitors

Your content can be quoted inside two billion AI answers a month and still send zero visitors. That is not a traffic problem, it is a measurement problem, and the old dashboard cannot see it.

read_post →

How to build video that AI search actually cites

YouTube is the most-cited source in Google's AI Overviews, and short-form is where product discovery now begins. What it takes to make your videos the ones AI search pulls from.

read_post →

In Google's AI Mode, the source getting cited most is Google itself

A study of 50,000 commercial keywords found Google has become the second most-cited source inside its own AI Mode, by pulling from its own Business Profiles and Knowledge Panels. That rewrites the local SEO playbook.

read_post →